It’s no secret that primary care is the keystone of effective, efficient care delivery. The primary care workforce is the beating heart of the system and a number of recent publications have shed additional light on how it is changing over time. The National Center for Health Workforce Analysis published The State of the Primary Care Workforce which calls additional attention to the need to build up the primary care workforce nationally.

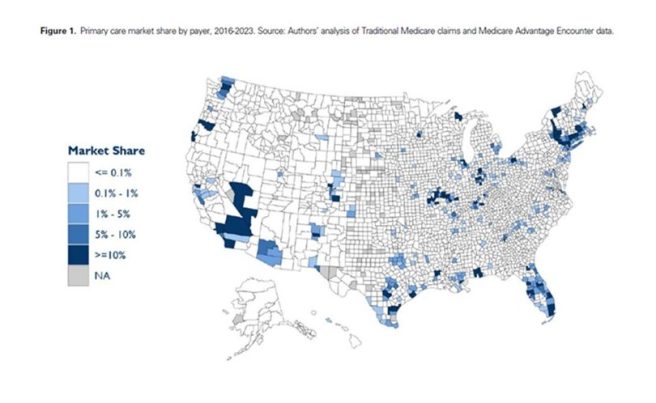

In addition, Adler, Crow, et. al. published a wonderful piece in the June 11th edition of Health Affairs Scholar that sheds light on payer-primary care integration. They use data through 2023 so it is possible that their estimates may be understated. They find that payer-operated practices account for 4.2% of the national primary care market by service volume in 2023, up from 0.78% in 2016. It’s not clear yet what the implications will be from these arrangements in the long term, but it is interesting to see how the magnitude of payer-owned practices is concentrated largely in select regions of the nation. The authors note a direct relationship of more payer-owned practices in regions with higher Medicare Advantage penetration.

The authors include an interesting geographic representation of the magnitude of payer ownership of primary care practices throughout the nation. For Michigan, the regions with concentration are in Marquette, southeast Michigan, and Grand Rapids. For an additional perspective on payer ownership of primary care practices in the Midwest, consider that there are no counties in Michigan where payer-owned primary care represents 10% or more of the primary care market, but one county in Ohio (Summit) and one in Illinois (Cook) do. Take a look at how rates compare across the country: