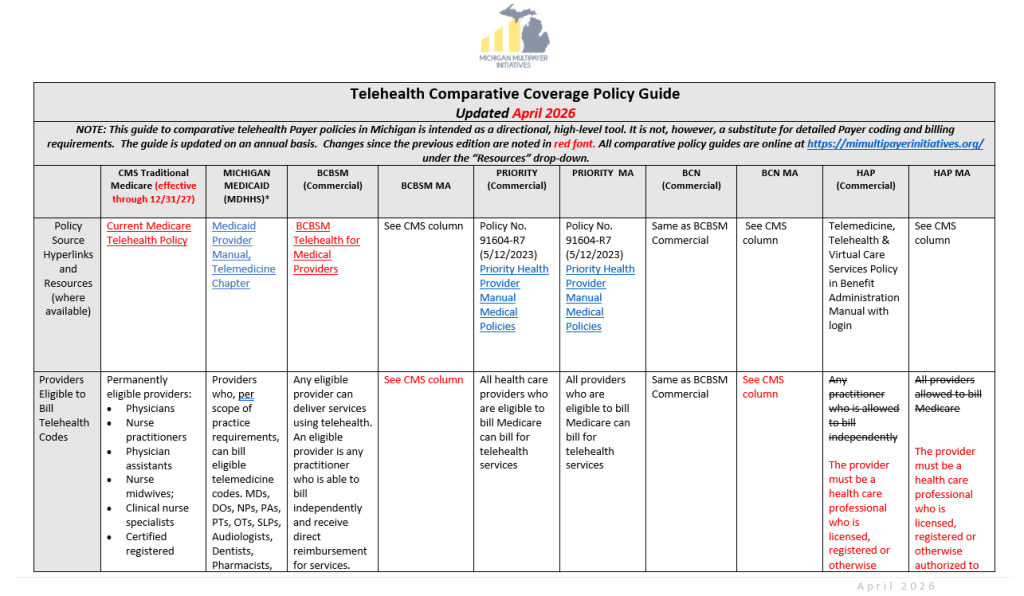

Updated 2026 Version of Telehealth Comparative Payer Policy Table

It’s available! Our payer leaders have worked with us to produce the latest update of a comparative payer policy and coverage table that provides a high-level guide to payer approaches for billing and coding of telehealth services. You’ll see substantial alignment with CMS traditional policy as well as policy source link, where available. Though the incentive table does not replace Individual in-depth payer detail, it serves as a tool to reduce confusion and decrease administrative burden for busy primary care practices.

2026 Telehealth Comparative Payer Policy Table

Implementing the CMS Advanced Primary Care Management (APCM) Codes: Learning from the Leaders

In 2025, CMS introduced Advanced Primary Care Management (APCM) services to recognize and reimburse the ongoing, often invisible work primary care practices perform between office visits. The codes function as monthly bundled payments designed to support practices that provide comprehensive, relationship-based primary care.

To reduce administrative burden, unlike the Chronic Care Management (CCM) and Principal Care Management (PCM) codes, APCM codes are not time-based, an additional benefit of the codes. They can be used across the array of Traditional Medicare patients in a panel and the three base APCM codes — G0556, G0557, and G0558 — vary by the complexity of the patient. In 2026, CMS built on the APCM code chassis by launching behavioral health APCM add-on codes, G0568 (Initial/first month of Psychiatric Collaborative Care Management (CoCM) services); G0569 (Subsequent months of Psychiatric Collaborative Care Management (CoCM) services); and G0570 (General Behavioral Health Integration (BHI) services).

Because of the structure of Traditional Medicare, the codes bear a 20% cost share. However, the vast majority (about 90%) of Traditional Medicare patients also purchase a Medicare supplementary policy to absorb these costs. Despite this, having even a small portion of patients who are not protected from cost-sharing has slowed the adoption of the APCM codes. However, there are early adopter advanced primary care practices who have demonstrated that successful implementation of APCM codes depends less on adding new clinical work and more on documenting and organizing work practices are already doing, and that open communication with patients is the key to consent and partnership.

The Primary Care Collaborative’s April 28, 2026 webinar, Advanced Primary Care Management: Successful Adopters Tell Their Stories, provided insight from leading practices across the nation who are successfully using APCM codes. The Collaborative will also be devoting its 2026 evidence report to exploring the impact of APCM codes and estimating the expense of waiving the cost-share. The premise is that if greater adoption of APCM produces better outcomes for CMS then removing the patient cost share would be a wise investment.

Advanced Primary Care Management (APCM) Code Basics

CMS designed APCM to incorporate elements of:

- Chronic Care Management (CCM)

- Principal Care Management (PCM)

- Transitional Care Management (TCM)

- Virtual check-ins

- Digital communications

- Care coordination activities

Practices do not need to provide every APCM element every month. CMS states that required elements must be completed “as clinically appropriate.”

CMS enabled three APCM codes stratified by patient complexity:

- G0556 — Patients with one or fewer chronic conditions

- G0557 — Patients with two or more chronic conditions

- G0558 — Qualified Medicare Beneficiaries (QMBs) with two or more chronic conditions

APCM codes can be billed once per patient per calendar month but cannot be billed concurrently with overlapping codes including transitional care management or complex care management.

The PCC webinar tells the APCM implementation story of Dr. Jason Lofton from Lofton Family Clinic in Arkansas who has 500 Medicare patients. Dr. Lofton has found APCM easier to implement and bill than Chronic Care Management codes and his preliminary data indicates that decreases in both inpatient utilization and emergency department utilization from APCM use. Dr. Lofton’s practice schedules the majority of Annual Wellness Visits (AWV) in January and February and uses it as an opportunity to explain the APCM concept and gain patient consent and finds the majority of his patients are very responsive.

Dr. Sam Hiatt of Community Care of North Carolina (CCNC), a clinically integrated network that provides the lease of pharmacists, nurses, and other clinicians, to practices, especially for practices whose panels are too small to be able to hire resources outright but would benefit from a partial resource. CCNC focuses on delivering a partnership care team model, especially for rural practices who report that the leased resources are helpful in enabling them to improve outcomes and performance in shared savings models. They also have been helpful in fulfilling the servicing requirements of the APCM codes.

The early adopters who have integrated APCM into their workflows and billing processes also shared some advice for others exploring operationalizing APCM codes. If a practice is already performing population health management, portal messaging, medication reconciliation, and care coordination, it is closer to APCM readiness than it may realize.

Release of Michigan State Medical Society’s Subcommittee on Physician Workforce Recommendations Report

If you haven’t yet come across the Michigan State Medical Society’s new report on Physician Workforce Recommendations, it is more than worth the read. The report is a culmination of 18 months of effort and focuses on four key areas: 1) Reforming primary care payment; 2) Reducing systemwide administrative burden; 3) Reimagining the training and education of primary care physicians; and 4) Improving the recruitment and retention of primary care physicians to practice in Michigan.

The report was covered in both Bridge Michigan and the Washington Post, in no small part because of its focus on the consensus that high-quality primary care is the foundation for patient-centric, coordinated, and cost-effective care.

The recommendations urge the following actions on primary care payment reform:

- Pass a legislative primary care spending target in Michigan of 12% of total medical expenditures, so primary care physicians can fund care teams of RN Care Managers, advanced practice providers (NPs/PAs), physicians, and auxiliary providers as appropriate for the practice panel;

- All payers (Medicaid, commercial, etc.) should transition their primary care payment models to a hybrid primary care payment mode; and

- Encourage systems, physician organizations, and similar entities to sign on to a voluntary compact to channel enhanced primary care investment funding to the practice level, ensuring practices can resource teams.

The recommendations for other areas are just as action-oriented and relevant. Read on here for the complete set.

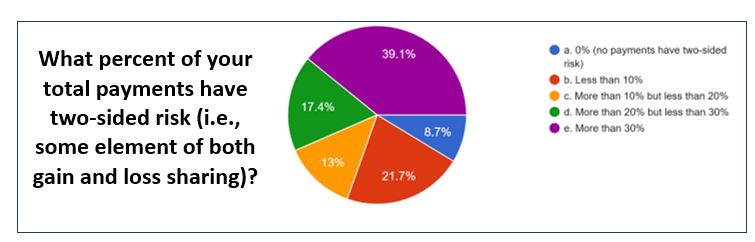

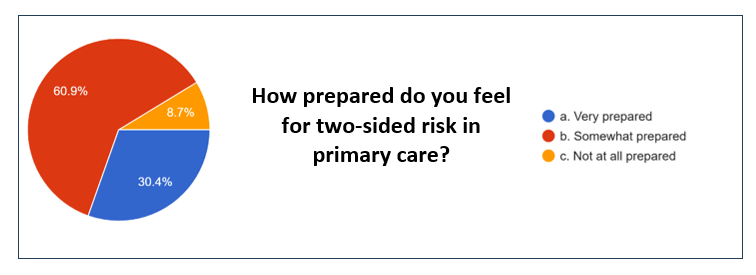

2026 Michigan Multipayer Initiatives Physician Organization Primary Care Survey Results

Our thanks to the 23 Physician Organizations (POs) that took time to respond to the Michigan Multipayer Initiatives 2026 PO survey. In addition to the standing questions from previous years, this year’s version also included questions on Advanced Primary Care (APC) implementation and value-based payment approaches.

Drumroll….here are the results. In a nutshell:

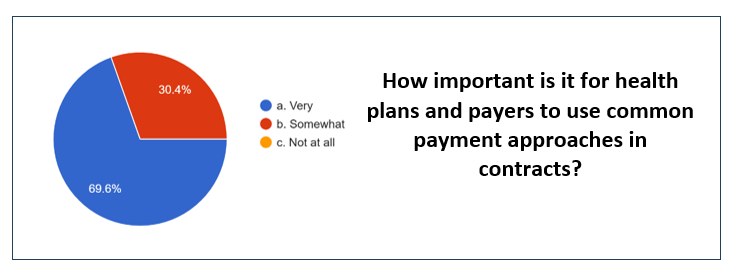

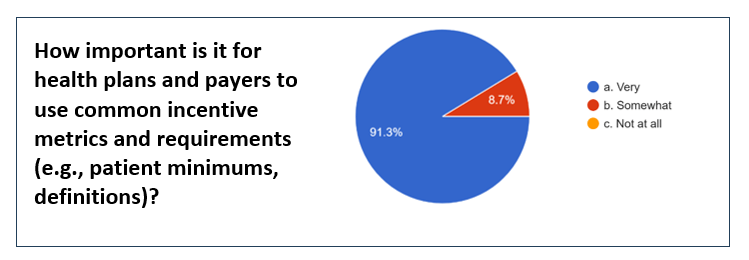

- POs expressed a strong interest in incentive alignment among payers;

- Most feel somewhat or very prepared for two-sided risk;

- Well over half of the responding POs have at least 20% of their payments in two-sided risk;

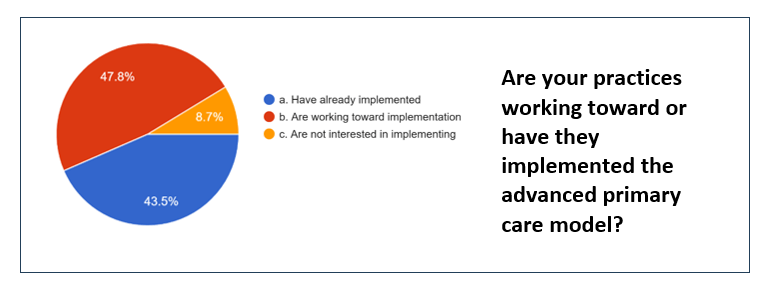

- Over 90% of POs report that their practices have either fully implement or are in the process of implementing Advanced Primary Care (APC).

Read along with the Primary Care Review community!

Growth in National Health Expenditures: It’s the Prices, Stupid

Mike Chernew is an accomplished health economist who has served as MedPac Chair and has made many excellent contributions to the literature and to applied health policy. His recent Health Affairs article, “Growth in National Health Expenditures: It’s Not the Prices, Stupid,” is no exception. He translates the 2024 National Health Expenditures (NHE) findings into everyday language we can all understand. The 2024 NHS report showed a 7.2% growth rate in 2024, just a tad down from 2023’s 7.4% growth. Chernew emphasizes that intensity and volume are the primary drivers that serve to increase health expenditures. Other contributors to the upward trend are the use of low value services, shifts to higher-priced settings, growth in coding intensity, and the use of more expensive drugs. Chernew concludes that continuing to spend at this rate is not affordable as the tax and wage pressures to finance it are extreme. He notes that we can’t cost-shift the problem away, either. Importantly, he doesn’t just talk about the problem; he suggests some recommendations:

- Focusing on strategies to reduce low-value care and inappropriate coding in fee-for-service settings

- Improving designs of alternative payment models (APM) that create incentives for providers to practice efficiently, including improved benchmark-setting rules and risk adjustment

- Regulating areas where markets fail (price regulation, standardization to support patient choice, simplification of administratively burdensome regulations

- Improving market mechanisms to induce more efficient care-seeking behavior